Every 2026 Launch at a Glance

Over twenty new condo launches are confirmed or highly likely for 2026 across all regions. Six projects launched in Q1 (January to March), at least six more are confirmed for Q2 (April to June), and the second half brings mega-developments alongside a significant wave of ECs and CCR entries.

| Project | Units | District | Est. PSF | Launch |

|---|---|---|---|---|

| Coastal Cabana EC | 748 | D18 | $1,734 avg | Jan 2026 |

| Newport Residences | 246 | D2 | $3,370 avg | Jan 2026 |

| Narra Residences | 540 | D23 | $2,180 avg | Jan 2026 |

| River Modern | 455 | D9 | $3,266 avg | Mar 2026 |

| Pinery Residences | 588 | D18 | ~$2,340 | Mar 2026 |

| Rivelle Tampines EC | 572 | D18 | TBA | Mar 2026 |

| 132 Sophia Road | 40 | D9 | $2,800+ | Q1/Q2 2026 |

| Vela Bay | 515 | D16 | $2,500-$2,800 | Apr VVIP |

| Tengah Garden Residences | ~860 | D24 | $1,600-$2,000 | Apr VVIP |

| Hudson Place Residences | ~325 | D5 | ~$2,200+ | Q2 2026 |

| Lentor Gardens Residences | 499 | OCR | $2,200+ | Q2 2026 |

| Chencharu Close | ~875 | D27 | $1,750-$2,000 | Mid 2026 |

| Lakeside Drive (Lakeside Grand) | ~575 | D22 | $2,300-$2,500 | Q2/Q3 2026 |

| Dorset Road Residences | ~428 | D8 | $2,500-$2,750 | Q3 2026 |

| Thomson View | ~1,240 | D20 | $2,300-$2,600 | Mid-late 2026 |

| Chuan Grove | ~1,055 | D19 | $2,600-$2,800 | Q3/Q4 2026 |

| Lentor Central (Plot 4) | ~580 | D26 | $2,400-$2,700 | H2 2026 |

| Hougang Central Residences | ~835 | D19 | $2,200-$2,500 | H2 2026 |

| Holland Link | ~235 | D10 | Above $2,800 | H2 2026 |

| Dunearn Road Condo | ~370 | D10/11 | $2,700-$3,000 | H2 2026 |

| Upper Thomson Rd (Parcel A) | ~595 | D26 | $2,200-$2,300 | Q4 2026 |

| Senja Close EC | 295 | D23 | TBA | Q4 2026 |

| Telok Blangah Road | ~745 | D4 | $2,500-$2,800 | ~Nov 2026 |

| Bukit Timah Road (Newton) | ~340 | D11 | $3,000+ | Late 2026 |

| Sembawang Road EC | ~265 | D27 | TBA | Late 2026 |

| Woodlands Drive 17 EC | ~980 | D25 | $1,750-$2,000 | Late 2026 |

| Keppel Bay Plot 6 | 86 | D4 | TBA (premium) | 2026 (TBC) |

Market Context

Three forces define 2026: record GLS land bids (Bayshore Road at $1,388 psf ppr, Dorset Road at $1,338 psf ppr with nine bidders), tight supply (URA projects 6,000 to 7,000 completions vs ERA's forecast of 9,000 to 10,000 new home sales), and upgraded SSD rules extending the holding period to four years with a 16% top rate. Price floors are structurally supported. Do not expect meaningful discounts.

Price Benchmarks

| Region | New Launch PSF Range | Recent Benchmarks |

|---|---|---|

| CCR | $2,800 to $3,300+ | Robertson Opus ~$3,360, UpperHouse ~$3,350 |

| RCR | $2,400 to $2,800 | The Orie $2,704, Elta $2,537 |

| OCR | $1,800 to $2,360 | Parktown $2,360, Lentor Central ~$2,200 |

| EC | $1,650 to $1,770 | Aurelle $1,766, Coastal Cabana $1,734 |

The CCR-to-OCR premium has compressed to just 7% (PropNex Q1 2025 data). Some RCR launches are pricing at or above CCR levels.

Key Matchups

- Vela Bay vs Lakeside Drive: East Coast lifestyle now vs Jurong Lake District future. Owner-occupiers lean Vela Bay; long-horizon investors lean Lakeside.

- Thomson View vs Chuan Grove: Value play with CRL interchange upside vs established Serangoon neighbourhood safety. Match to client risk appetite.

- Hudson Place vs Dover Road: Both in one-north corridor. Hudson Place for certainty; Dover Road for comparison if clients can wait.

- Tengah Garden vs Lentor Gardens: Lowest quantum (Tengah, $1,600+) vs proven demand (Lentor, $2,200+).

Risks to Watch

- Q3 clustering: Thomson View (~1,240 units), Chuan Grove (~1,055 units), and Hougang Central (~835 units) all launching in the same quarter. Over 3,000 units competing for buyers could soften individual take-up rates.

- Interest rate sensitivity: Stress-test clients at 3.5% to 4% rates, not just current 1.5% to 2%.

- Global headwinds: Singapore's safe-haven status historically attracts capital during uncertainty, but advise clients to buy within their means.

Key Takeaways

- Q2 2026 brings at least five launches, led by Vela Bay and Tengah Garden (both VVIP in April).

- Q3 and beyond features mega-developments plus the first private launch on the Greater Southern Waterfront (Telok Blangah Road).

- Three ECs launching in H2 2026 and early 2027: Senja Close, Sembawang Road, and Woodlands Drive 17.

- CRL Phase 1 (2030) is the next major connectivity catalyst, creating a TEL-CRL interchange at Bright Hill.

- Pre-register at showflats, segment your client list, and prepare comparison talking points before launch day.

Switch to Detailed view above for the full analysis, including individual project profiles with developer details, MRT connectivity tables, head-to-head positioning tips, tax rate references, and FAQ.

Launch season is here. ERA projects 18 private residential developments and 5 EC projects for the whole of 2026, with a heavy concentration of launches in Q2 and Q3. Several of the largest projects are confirmed for this window, making it the busiest launch season in recent years.

This cheat sheet covers every confirmed and likely 2026 launch, verified pricing benchmarks, head-to-head comparisons, buyer profiles by project, MRT connectivity plays, and the market risks you should be ready to discuss with clients.

Bookmark this. You will need it.

TL;DR: Every 2026 Launch at a Glance

Over twenty projects are confirmed or highly likely for 2026, with six already launched in Q1. Here is every project at a glance.

| Project | Units | District | Developer | Tenure | Est. PSF | Launch | Best For |

|---|---|---|---|---|---|---|---|

| Coastal Cabana EC LAUNCHED | 748 | D18 (Pasir Ris) | Qingjian / Forsea | 99-yr EC | $1,734 avg | Jan 2026 | East-side EC upgraders |

| Newport Residences LAUNCHED | 246 | D2 (CBD) | CDL | Freehold | $3,370 avg | Jan 2026 | CBD luxury, freehold investors |

| Narra Residences LAUNCHED | 540 | D23 (Dairy Farm) | Santarli / Apex Asia | 99-yr | $2,180 avg | Jan 2026 | Nature-focused families |

| River Modern LAUNCHED | 455 | D9 (River Valley) | GuocoLand | 99-yr | $3,266 avg | Mar 2026 | CCR riverfront lifestyle |

| Pinery Residences LAUNCHED | 588 | D18 (Tampines) | Hoi Hup / Sunway | 99-yr | From $2,340 | Mar 2026 | Tampines families, MRT integrated |

| Rivelle Tampines EC LAUNCHED | 572 | D18 (Tampines) | Sim Lian | 99-yr EC | TBA | Mar 2026 | First EC in Tampines West |

| 132 Sophia Road | 40 | D9 (Mt Sophia) | Sin Thai Hin | 103-yr | $2,800+ | Q1/Q2 2026 | CCR boutique buyers, PRs |

| Vela Bay | 515 | D16 (Bayshore) | SingHaiyi-Garnet JV | 99-yr | $2,500-$2,800 | Apr 2026 VVIP | East Coast lifestyle buyers |

| Tengah Garden Residences | ~860 | D24 (Tengah) | Hong Leong / GuocoLand / CSC | 99-yr | $1,600-$2,000 | Apr 2026 VVIP | First-timers, budget upgraders |

| Hudson Place Residences | ~325 | D5 (one-north) | Qingjian Realty JV | 99-yr | ~$2,200+ | Q2 2026 | Investors (tech rental demand) |

| Lentor Gardens Residences | 499 | OCR (Lentor) | Kingsford Group | 99-yr | $2,200+ | Q2 2026 | Thomson corridor upgraders |

| Chencharu Close | ~875 | D27 (Yishun) | Evia / Gamuda / Ho Lee | 99-yr | $1,750-$2,000 | Mid 2026 | Khatib MRT, integrated hub |

| Lakeside Drive (Lakeside Grand) | ~575 | D22 (Jurong) | CDL | 99-yr | $2,300-$2,500 | Q2/Q3 2026 | Long-horizon JLD investors |

| Dorset Road Residences | ~428 | D8 (Farrer Park) | UOL / SingLand / Kheng Leong | 99-yr | $2,500-$2,750 | Q3 2026 | City-fringe rental yield |

| Thomson View | ~1,240 | D20 (Bright Hill) | UOL / SingLand / CapitaLand | 99-yr | $2,300-$2,600 | Mid-late 2026 | Upgraders, CRL interchange play |

| Chuan Grove | ~1,055 | D19 (Lorong Chuan) | Sing Holdings / Sunway | 99-yr | $2,600-$2,800 | Q3/Q4 2026 | Serangoon families, upgraders |

| Lentor Central (Plot 4) | ~580 | D26 (Lentor) | GuocoLand / Intrepid / TID | 99-yr | $2,400-$2,700 | H2 2026 | Lentor cluster, upgraders |

| Hougang Central Residences | ~835 | D19 (Hougang) | CapitaLand / UOL Group | 99-yr | $2,200-$2,500 | H2 2026 | NEL/CRL interchange, integrated living |

| Holland Link | ~235 | D10 (Holland) | Sim Lian | 99-yr | Above $2,800 | H2 2026 | Low-rise CCR, Holland corridor |

| Dunearn Road Condo | ~370 | D10/11 (Turf City) | Frasers / Sekisui / CSC | 99-yr | $2,700-$3,000 | H2 2026 | Turf City transformation, CCR families |

| Upper Thomson Rd (Parcel A) | ~595 | D26 (Springleaf) | Wee Hur / GSC | 99-yr | $2,200-$2,300 | Q4 2026 | TEL access, nature corridor |

| Senja Close EC | 295 | D23 (Bukit Panjang) | CDL | 99-yr EC | TBA | Q4 2026 | EC buyers, DTL access |

| Telok Blangah Road | ~745 | D4 (GSW) | Kingsford Huray | 99-yr | $2,500-$2,800 | ~Nov 2026 | Greater Southern Waterfront early entry |

| Bukit Timah Road (Newton) | ~340 | D11 (Newton) | HH Investment | 99-yr | $3,000+ | Late 2026 | CCR premium, Newton MRT |

| Sembawang Road EC | ~265 | D27 (Sembawang) | Oriental Pacific | 99-yr EC | TBA | Late 2026/Q1 2027 | Possibly Singapore's first low-rise EC |

| Woodlands Drive 17 EC | ~980 | D25 (Woodlands) | CDL / Sim Lian | 99-yr EC | $1,750-$2,000 | Late 2026/early 2027 | Northern EC upgraders, TEL access |

| Keppel Bay Plot 6 | 86 | D4 (Keppel Bay) | Keppel Land | 99-yr | TBA (premium) | 2026 (TBC) | Boutique waterfront, GSW |

Also on the radar: Dover Road (~625 units, D5, details emerging)

What's Driving Launch Season 2026

Three forces are shaping this cycle. Elevated land costs, tight supply, and upgraded stamp duty rules are combining to create a market where preparation is everything.

Elevated land costs are locking in higher PSF floors. GLS land bids throughout 2024 and 2025 came in at record levels. The Bayshore Road site went for $1,388 psf ppr. Dorset Road drew nine bidders and closed at $1,338 psf ppr. These land costs, combined with construction costs that have risen significantly over the past decade, mean new launch prices have structural support. Do not expect meaningful discounts.

Supply remains tight. According to URA data, around 6,100 private homes (excluding ECs) were completed in 2025. Projected completions for 2026 sit around 6,000 to 7,000 units, still below historical averages. ERA projects 9,000 to 10,000 new home sales in 2026, signalling strong demand against limited supply.

Upgraded SSD rules are reshaping buyer behaviour. Since July 2025, the Seller's Stamp Duty holding period extends to four years (up from three), with rates increasing by four percentage points per tier. The top rate for selling within year one is now 16%. This will push more buyers toward genuine owner-occupier and long-hold investor profiles, reducing speculative demand.

Q1 2026: Already Launched

Six projects launched in Q1 2026 (January to March). Here is a quick recap of each, including launch performance where available.

| Project | Units | District | Avg PSF | Launch | Take-up |

|---|---|---|---|---|---|

| Coastal Cabana EC | 748 | D18 (Pasir Ris) | $1,734 | Jan 17 | 67% on launch weekend |

| Newport Residences | 246 | D2 (CBD, Freehold) | $3,370 | Jan 31 | 57% on launch weekend |

| Narra Residences | 540 | D23 (Dairy Farm) | $2,180 | Jan 31 | ~25% on launch weekend |

| River Modern | 455 | D9 (River Valley) | $3,266 | Mar 7 | 90% on launch day |

| Pinery Residences | 588 | D18 (Tampines) | From ~$2,340 | Mar 28 | Just launched |

| Rivelle Tampines EC | 572 | D18 (Tampines) | TBA | Mar 21 | Just launched |

Key takeaway from Q1: Strong demand across all segments. River Modern's 90% take-up at $3,266 psf in the CCR and Coastal Cabana's 67% at $1,734 psf in the EC segment both signal robust buyer appetite heading into Q2. Notably, Q1 saw Tampines receive two simultaneous launches (Pinery Residences and Rivelle Tampines EC), creating direct competition in the same precinct.

Q2 2026 Launches (April to June)

At least five projects are confirmed or likely for Q2 2026, led by two VVIP previews in April. Here is every project with verified details.

Vela Bay

| Units | 515 (two 31-storey towers) |

| Location | Bayshore Road, District 16 |

| Developer | SingHaiyi Group & Haiyi Holdings (SingHaiyi-Garnet JV) |

| Tenure | 99-year leasehold |

| Est. PSF | $2,500 to $2,800 |

| Launch | VVIP Preview 11 April 2026 |

| TOP | Est. 2030 |

Why it matters: This is the first private residential launch in the Bayshore precinct in over 25 years. The site sits adjacent to Bayshore MRT (TE29) on the Thomson-East Coast Line, which opened in June 2024. TEL Stage 5, adding Bedok South (TE30) and Sungei Bedok (TE31), is expected to open in H2 2026, further boosting the area's connectivity.

Key selling points: Direct MRT access, proximity to East Coast Park, the upcoming Bayshore integrated development (1,280 units with commercial and community spaces), and the area's transformation under the URA Master Plan.

Best buyer profile: Owner-occupiers who want East Coast lifestyle with MRT convenience. Also appeals to investors eyeing the area's long-term transformation upside.

Tengah Garden Residences

| Units | ~860 (mid-rise blocks up to 16 storeys, with commercial) |

| Location | Tengah Garden Avenue, District 24 |

| Developer | Hong Leong Holdings, GuocoLand & CSC Land Group |

| Tenure | 99-year leasehold |

| Est. PSF | $1,600 to $2,000 |

| Launch | VVIP Preview April 2026 |

Why it matters: This is the first private condo in Tengah, Singapore's "Forest Town." The development is mixed-use with ground-floor commercial space. It is near the upcoming Hong Kah MRT station on the Jurong Region Line.

Key selling points: Lowest entry price among Q2 launches, brand-new town infrastructure, green town concept with car-lite features, and developer pedigree (Hong Leong + GuocoLand).

Best buyer profile: First-time buyers and young families looking for affordable private entry points. HDB upgraders from Jurong, Bukit Batok, and Choa Chu Kang. Budget-conscious investors seeking quantum plays.

Hudson Place Residences

| Units | ~325 (two 23-storey towers with ground-floor commercial) |

| Location | Media Circle, one-north, District 5 |

| Developer | Qingjian Realty, Forsea Holdings & Hoovasun Holding |

| Tenure | 99-year leasehold |

| Est. PSF | ~$2,200+ (estimate based on land cost) |

| TOP | Est. 2030 |

Why it matters: Positioned in Singapore's innovation district alongside Biopolis, Fusionopolis, and Mediapolis. A short commute to one-north MRT on the Circle Line (complimentary shuttle service provided), and one stop from Buona Vista interchange (Circle Line + East-West Line).

Key selling points: Strong rental demand from the tech and biomedical professionals working in one-north. Proximity to NUS and NUH.

Best buyer profile: Investors targeting the rental market (tech professionals, researchers, NUS staff). Also suitable for owner-occupiers working in the one-north corridor.

Lentor Gardens Residences

| Units | 499 |

| Location | Lentor area (OCR) |

| Developer | Kingsford Group |

| Tenure | 99-year leasehold |

| Est. PSF | Above $2,200 |

| Launch | Q2 2026 |

Why it matters: The Lentor cluster has been one of the most active new launch zones in recent years. This project benefits from the lowest land cost among Lentor plots at ~$920 psf ppr, which could translate to competitive pricing.

Best buyer profile: Upgraders from Ang Mo Kio, Bishan, and Yishun HDB estates. Young families drawn to the Thomson corridor.

132 Sophia Road (Sophia Meadow)

| Units | 40 (boutique development) |

| Location | 132 Sophia Road, District 9 |

| Developer | Sin Thai Hin Development |

| Tenure | 103-year lease |

| Est. PSF | $2,800+ (estimated, not confirmed) |

| Launch | Q1/Q2 2026 |

Why it matters: A rare boutique CCR project in the Mount Sophia enclave. Walking distance to Dhoby Ghaut MRT (triple-line interchange: NSL, NEL, CCL) and Bencoolen MRT (DTL). Near Plaza Singapura and the Orchard Road belt.

Best buyer profile: High-net-worth owner-occupiers or investors looking for CCR entry at a smaller quantum. Possibly attractive to PRs seeking D9 addresses.

Also on the radar for Q2: Dover Road Mixed-Use Development (~625 units, D5, 99-year leasehold), about 250m from one-north MRT. Details still emerging. Bloomsbury Residences (358 units, D5, one-north, Qingjian Realty JV) launched earlier in 2026 at $2,474 avg PSF and is already selling.

Managing prospects across multiple launches?

Track who is interested in what, schedule follow-ups, and never miss a lead during launch season.

Try PropPal Free for 7 Days Setup takes 5 minutes. Cancel anytime.Q3 2026 and Beyond (July Onwards)

The second half of launch season brings the mega-developments alongside a significant wave of ECs and CCR entries. Thomson View (~1,240 units), Chuan Grove (~1,055 units), and Hougang Central Residences (~835 units) lead the pack, with Telok Blangah Road (~745 units) marking the first private launch on the Greater Southern Waterfront.

Lakeside Drive Condo (Lakeside Grand)

| Units | ~575 (1-BR+study to 5-BR, with ground-floor commercial) |

| Location | Lakeside Drive, District 22 |

| Developer | City Developments Limited (CDL) |

| Tenure | 99-year leasehold |

| Est. PSF | $2,300 to $2,500 |

| TOP | December 2030 |

Why it matters: Directly adjacent to Lakeside MRT (East-West Line) and sits within the Jurong Lake District, Singapore's planned second CBD. The broader CRL network will eventually serve this district, and the Jurong Region Line will eventually add another line to nearby Jurong East (originally targeted for 2028, now subject to delays). When complete, multiple MRT lines will converge in this district.

Best buyer profile: Long-horizon investors banking on the Jurong Lake District story. Owner-occupiers working in Jurong industrial or the future commercial hub.

Dorset Road Residences

| Units | ~428 (two 27-storey towers) |

| Location | Dorset Road / Owen Road, District 8 (Farrer Park) |

| Developer | UOL Group, Singapore Land Group & Kheng Leong |

| Tenure | 99-year leasehold |

| Est. PSF | $2,500 to $2,750 |

| Launch | Q3 2026 (confirmed target) |

Why it matters: District 8 straddles the RCR-CCR boundary. The GLS tender attracted nine bidders, among the highest bidder counts for any 2025 GLS site, signalling strong developer confidence in the location. Five minutes' walk to Farrer Park MRT (NEL).

Best buyer profile: Investors looking for city-fringe rental yield. PRs and singles who want urban convenience. Owner-occupiers who value nightlife and food culture proximity.

Thomson View (Redevelopment)

| Units | ~1,240 |

| Location | Bright Hill Drive, District 20 |

| Developer | UOL Group, Singapore Land Group & CapitaLand Development |

| Tenure | 99-year leasehold (fresh lease) |

| Est. PSF | $2,300 to $2,600 |

| Launch | Mid to late 2026 (could be Q3 or Q4) |

Why it matters: This is one of the largest en bloc redevelopments in recent years (former Thomson View estate, sold for $810 million). The site is near three MRT stations: Upper Thomson (TE8), Bright Hill (TE7), and Marymount (CCL). Critically, Bright Hill will become a TEL-CRL interchange when CRL Phase 1 opens in 2030, adding significant future connectivity.

Key selling points: Mega-development scale (likely competitive pricing), triple MRT access, CRL interchange upside, proximity to nature (MacRitchie, Lower Peirce), and a powerhouse developer consortium.

Best buyer profile: HDB upgraders from Ang Mo Kio, Bishan, and Toa Payoh. Families valuing schools in the Thomson corridor. Long-hold investors attracted by the CRL interchange catalyst.

Chuan Grove

| Units | ~1,055 (five blocks up to 27 storeys, with ancillary retail) |

| Location | Chuan Grove, Serangoon / Lorong Chuan, District 19 |

| Developer | Sing Holdings (65%) & Sunway Developments (35%) |

| Tenure | 99-year leasehold |

| Est. PSF | $2,600 to $2,800 |

| Launch | Q3 or Q4 2026 |

Important clarification: Chuan Grove is NOT the former Chuan Park. Chuan Park (by Kingsford/MCC, 916 units) launched separately in November 2024 and is already selling. Chuan Grove is a distinct project on two adjacent GLS sites.

Why it matters: Within 400m of Lorong Chuan MRT (Circle Line) and one stop from Serangoon MRT interchange (NEL + CCL). CRL Phase 1 will add Serangoon North station (CR9) by 2030, improving the area's connectivity further.

Best buyer profile: Families upgrading from Serangoon, Hougang, and Ang Mo Kio HDB estates. Owner-occupiers who value the mature Serangoon neighbourhood.

Hougang Central Residences

| Units | ~835 (integrated mixed-use development) |

| Location | Hougang Central, District 19 |

| Developer | CapitaLand Development, UOL Group & CapitaLand Integrated Commercial Trust (CICT) |

| Tenure | 99-year leasehold |

| Est. PSF | $2,200 to $2,500 (based on land cost of $1,179 psf ppr) |

| Launch | H2 2026 |

Why it matters: This is a landmark integrated development sitting directly above Hougang MRT station on the North-East Line. Hougang will become a dual-line interchange when the Cross Island Line opens, adding CRL connectivity by 2030. The development includes approximately 300,000 sqft of retail space (the largest mall in Hougang), a bus interchange, and community facilities. The $1.5 billion winning bid signals serious developer conviction.

Key selling points: Direct MRT access (NEL now, CRL by 2030), integrated retail and transport hub, CapitaLand and UOL pedigree, and a location in one of the most established HDB heartlands with strong upgrader demand. The last major private launch in Hougang was in 2018/2019 (Riverfront Residences and The Florence Residences), both now fully sold.

Best buyer profile: Hougang/Punggol/Sengkang HDB upgraders looking for integrated convenience, investors seeking rental demand from the established Hougang population, and buyers who want direct MRT interchange access.

Lentor Central (Plot 4)

| Units | ~580 |

| Location | Lentor Central, District 26 |

| Developer | GuocoLand, Intrepid Investments & TID Residential |

| Tenure | 99-year leasehold |

| Est. PSF | $2,400 to $2,700 (based on land cost of $1,278 psf ppr) |

| Launch | H2 2026 |

Why it matters: This is the final GLS plot in the Lentor cluster, and it comes with the highest land cost among all Lentor sites at $1,278 psf ppr. That land cost points to launch pricing above the $2,200 psf range set by earlier Lentor projects like Lentor Hills Residences and Lentor Central Residences. GuocoLand's involvement (the same developer behind Lentor Modern and Midtown Modern) signals confidence in the precinct's premium positioning.

Key selling points: Final opportunity in the Lentor new launch cluster, which has seen strong take-up across all previous launches. Approximately 650m from Lentor MRT (TEL), with established pedestrian connectivity through the Lentor Modern commercial podium. GuocoLand's track record in the precinct (Lentor Modern, Lentor Hills Residences) gives buyers confidence in design quality and estate planning. The Lentor precinct's identity as a mature, nature-rich neighbourhood is now established, reducing the "new town risk" that earlier buyers faced.

Best buyer profile: Upgraders from Ang Mo Kio, Bishan, and Yishun who missed earlier Lentor launches. Investors who have seen the strong resale performance of Lentor Modern and want exposure to the final plot. Families drawn to the Thomson corridor's school catchments and TEL connectivity.

Telok Blangah Road

| Units | ~745 |

| Location | Telok Blangah Road, District 4 (Greater Southern Waterfront) |

| Developer | Kingsford Huray Development |

| Tenure | 99-year leasehold |

| Est. PSF | $2,500 to $2,800 (based on land cost of $1,326 psf ppr) |

| Launch | ~November 2026 |

Why it matters: This is the first private residential project on the Greater Southern Waterfront, one of the most ambitious transformation zones in Singapore's URA Master Plan. The GSW stretches from Pasir Panjang to Marina East, and this site offers early entry into what will be a decades-long redevelopment story. Proximity to Telok Blangah MRT (Circle Line) and HarbourFront MRT (NEL + CCL).

Best buyer profile: Long-hold investors who want early exposure to the Greater Southern Waterfront transformation. Owner-occupiers drawn to the waterfront lifestyle and proximity to Sentosa and VivoCity.

Holland Link

| Units | ~235 (low-rise blocks) |

| Location | Holland Link, District 10 |

| Developer | Sim Lian Group |

| Tenure | 99-year leasehold |

| Est. PSF | Above $2,800 (based on land cost of ~$1,432 psf ppr) |

| Launch | H2 2026 (showflat under construction) |

Why it matters: A low-rise development in the Holland/Bukit Timah estate, one of Singapore's most established residential enclaves. The showflat is under construction and the developer is targeting an H2 2026 launch. Proximity to Holland Village MRT (Circle Line) and the upcoming Holland Village extension.

Key selling points: Low-rise, low-density CCR living in one of Singapore's most sought-after residential enclaves. Walking distance to Holland Village's dining and lifestyle precinct. Near top international schools (United World College, Tanglin Trust, ISS International). Close proximity to Bukit Timah Nature Reserve and the Rail Corridor for nature access. Sim Lian's track record with similar mid-scale projects gives buyers confidence in delivery.

Best buyer profile: High-net-worth owner-occupiers seeking a low-rise, low-density lifestyle in the Holland corridor. Families who value the proximity to international schools and Holland Village amenities. Expatriate families on local packages looking for a CCR address near major international schools.

Bukit Timah Road (Newton)

| Units | ~340 |

| Location | Bukit Timah Road, District 11 (Newton) |

| Developer | HH Investment (Taiwan's Huang Hsiang Construction) |

| Tenure | 99-year leasehold |

| Est. PSF | $3,000+ (based on record land cost of $1,820 psf ppr) |

| Launch | Late 2026 to early 2027 |

Why it matters: This site was purchased at $1,820 psf ppr, the highest CCR GLS land price since 2018, which will translate to premium launch pricing. It is the first residential site in the new Newton neighbourhood under the URA Draft Master Plan 2025. Near Newton MRT (NSL + DTL interchange) and the upcoming Newton food centre area.

Key selling points: Dual-line MRT interchange access at Newton station (NSL + DTL), placing residents within 10 minutes of Orchard Road, Marina Bay, and the CBD. The record land cost signals that the developer views Newton as a premium CCR precinct with staying power. Proximity to Anglo-Chinese School (Barker Road), Singapore Chinese Girls' School, and other popular primary schools. The Newton food centre precinct and Stevens Road dining belt provide lifestyle amenities. Central location with easy access to CTE and PIE expressways.

Best buyer profile: High-net-worth buyers and investors seeking CCR addresses. Buyers attracted to the Newton precinct's centrality and dual-line MRT interchange access. Parents who want proximity to popular primary schools in the Newton/Novena zone.

Sembawang Road EC

| Units | ~265 |

| Location | Sembawang Road, District 27 |

| Developer | Oriental Pacific Holdings |

| Tenure | 99-year EC |

| Est. PSF | TBA |

| Launch | Late 2026 to Q1 2027 |

Why it matters: This could be Singapore's first low-rise EC development, which would make it unique in the market. The smaller unit count (265 units) and low-rise format appeal to buyers who prefer a boutique living environment. Near Sembawang MRT (NSL).

Best buyer profile: EC-eligible buyers in the north (Sembawang, Yishun, Woodlands) who want something different from the typical high-rise EC. Buyers who value lower density and a smaller community feel.

Dunearn Road Condo (Dunearn House)

| Units | ~370 |

| Location | Dunearn Road / Turf City, District 10/11 |

| Developer | Frasers Property, Sekisui House & CSC Land Group |

| Tenure | 99-year leasehold |

| Est. PSF | $2,700 to $3,000 (based on land cost of ~$1,410 psf ppr) |

| Launch | H2 2026 |

Why it matters: The first private residential project within the Turf City transformation zone. URA's plans for Turf City include a mix of residential, commercial, and recreational uses, turning the former racecourse area into a new neighbourhood. The site is next to Sixth Avenue MRT (DTL) and the future Turf City MRT station on the Cross Island Line.

Key selling points: First-mover advantage in a brand-new precinct with long-term transformation upside (similar to how early buyers in Paya Lebar Quarter benefited from district-level change). Walking distance to Sixth Avenue MRT (DTL) with future Turf City CRL station adding a second line. Proximity to elite schools including Hwa Chong Institution, National Junior College, and Methodist Girls' School. Direct access to Bukit Timah Nature Reserve and the Dairy Farm Nature Park connector. Low-rise format (five blocks up to 10 storeys) appeals to families who value space and greenery. Developer pedigree: Frasers Property, Sekisui House (Japan), and CSC Land Group.

Best buyer profile: CCR buyers attracted to the Bukit Timah corridor. Families valuing proximity to top schools (Hwa Chong, National Junior College) and nature (Bukit Timah Nature Reserve). Investors interested in the Turf City transformation upside, especially with the CRL station adding future connectivity.

Senja Close EC

| Units | 295 |

| Location | Senja Close, District 23 (Bukit Panjang) |

| Developer | City Developments Limited (CDL) |

| Tenure | 99-year EC |

| Est. PSF | TBA |

| Launch | Q4 2026 |

Why it matters: Located near Bukit Panjang MRT (Downtown Line + LRT interchange), this EC benefits from established Bukit Panjang amenities including Junction 10 mall and Hillion Mall. CDL's track record with ECs (including the upcoming Woodlands EC) gives buyers confidence in build quality and design.

Best buyer profile: EC-eligible buyers from the Bukit Panjang, Choa Chu Kang, and western corridor HDB estates. Families who value DTL access for commutes to the CBD and one-north.

Woodlands Drive 17 EC

| Units | ~980 (across two parcels) |

| Location | Woodlands Drive 17, District 25 |

| Developer | CDL (one parcel) and Sim Lian (one parcel) |

| Tenure | 99-year EC |

| Est. PSF | $1,750 to $2,000 |

| Launch | Late 2026 to early 2027 |

Why it matters: This is one of the largest EC launches coming to market, split across two adjacent parcels developed by two separate developers. Near Woodlands South MRT (Thomson-East Coast Line). The scale of this launch will provide ample supply for the underserved northern EC market, where demand from Woodlands, Admiralty, and Sembawang upgraders remains strong.

Best buyer profile: EC-eligible HDB upgraders from the northern corridor (Woodlands, Admiralty, Sembawang, Yishun). Buyers who want TEL access for faster commutes to the city. For more on ECs launching in 2026, see our Rivelle Tampines EC guide.

Chencharu Close

| Units | ~875 (integrated mixed-use with bus interchange and hawker centre) |

| Location | Chencharu Close, District 27 (Yishun/Khatib) |

| Developer | Evia Real Estate, Gamuda Land & Ho Lee Group |

| Tenure | 99-year leasehold |

| Est. PSF | $1,750 to $2,000 |

| Launch | Mid 2026 |

Why it matters: The first private project in the new Chencharu estate, a three-minute walk from Khatib MRT (NSL). This is an integrated development with a bus interchange and hawker centre built into the project. The site is part of a larger precinct plan for approximately 10,000 homes by 2040. The last condo launched in Yishun was The Essence in 2019, so there is significant pent-up demand in the area.

Best buyer profile: Upgraders from Yishun, Sembawang, and northern HDB estates. Buyers who value integrated convenience (transport hub, hawker centre, retail under one roof). Investors looking at the affordable OCR segment with strong rental demand from the northern population base.

Upper Thomson Road Parcel A

| Units | ~595 (mixed-use with ~2,000 sqm commercial) |

| Location | Upper Thomson Road, District 26 |

| Developer | Wee Hur Holdings & GSC Holdings |

| Tenure | 99-year leasehold |

| Est. PSF | $2,200 to $2,300 |

| Launch | Q4 2026 |

Why it matters: This is a separate project from Springleaf Residence (Parcel B by GuocoLand/Hong Leong), which launched earlier and achieved 92% sales at $2,177 psf average. That strong result validates demand in the precinct. Parcel A sits at the doorstep of Springleaf MRT (TEL) in a nature-rich setting near Thomson Nature Park and Lower Peirce Reservoir.

Best buyer profile: Upgraders from Ang Mo Kio, Yishun, and the Thomson corridor who want TEL access. Nature lovers drawn to the green surroundings. Buyers who saw Springleaf Residence sell out and want a second chance in the same precinct.

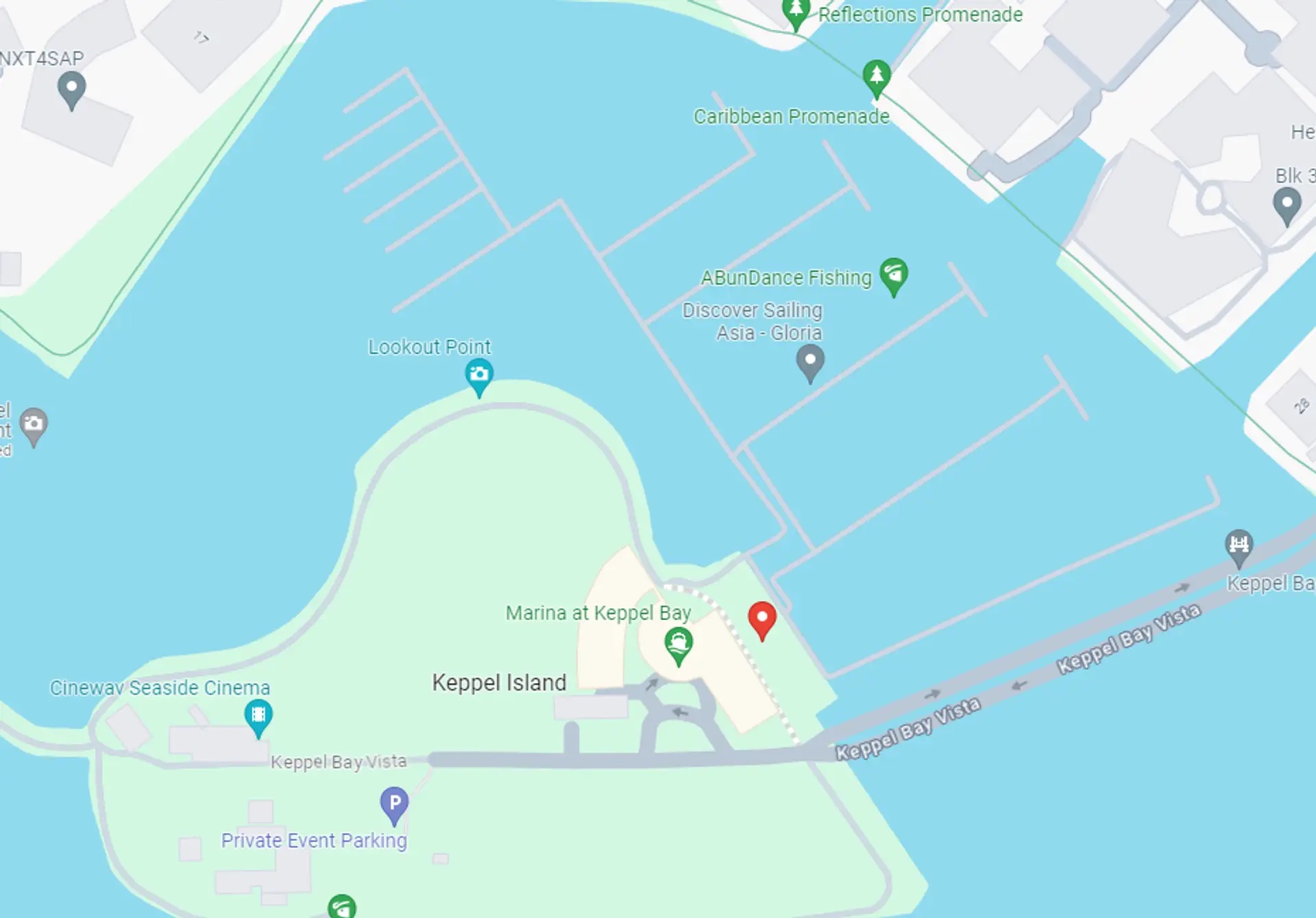

Keppel Bay Plot 6

| Units | 86 (boutique waterfront) |

| Location | Keppel Bay, District 4 |

| Developer | Keppel Land |

| Tenure | 99-year leasehold |

| Est. PSF | TBA (premium pricing expected) |

| Launch | 2026 (exact date unconfirmed) |

Why it matters: An exclusive 86-unit boutique waterfront development on Keppel Island, part of the Greater Southern Waterfront transformation. This is one of the most limited-supply launches of 2026. Near HarbourFront MRT (NEL + CCL) and a five-minute drive to the CBD. Marina views and resort-style amenities position this as a trophy asset play.

Key selling points: Extreme scarcity: only 86 units in the entire development, making it one of the smallest new launches in 2026. Waterfront living with marina views and direct access to Keppel Bay's boardwalk and marina. Neighbours include Reflections at Keppel Bay, Caribbean at Keppel Bay, and Corals at Keppel Bay, establishing the precinct's premium positioning. Keppel Land's track record as the precinct developer means integrated estate management. Proximity to HarbourFront MRT (dual-line interchange: NEL + CCL), VivoCity, and Sentosa. The Greater Southern Waterfront transformation will add significant amenities and infrastructure to this area over the next decade.

Best buyer profile: Ultra-high-net-worth buyers seeking a waterfront trophy property. Investors attracted to the Greater Southern Waterfront long-term story and the scarcity value of only 86 units. Buyers who value resort-style living with proximity to Sentosa, VivoCity, and the CBD.

Price Benchmarks: Where the Market Sits Today

New launch PSF prices have risen across all regions. Here are the current benchmarks based on recent transaction data and URA statistics, giving you the numbers you need for client conversations.

| Region | New Launch PSF Range | Recent Benchmarks |

|---|---|---|

| CCR | $2,800 to $3,300+ | The Robertson Opus (~$3,360 avg), UpperHouse (~$3,350 avg), River Green (~$3,130 avg) |

| RCR | $2,400 to $2,800 | The Orie at Toa Payoh ($2,704 avg), Elta at Clementi ($2,537 avg) |

| OCR | $1,800 to $2,360 | Parktown Residence ($2,360 avg), Lentor Central Residences (~$2,200 avg) |

| EC | $1,650 to $1,770 | Aurelle of Tampines ($1,766 avg), Coastal Cabana ($1,734 avg) |

Key trend to note: The price gaps between regions have narrowed to historic lows. According to PropNex data, the CCR premium over OCR compressed to just 7% in Q1 2025 (CCR median $2,554 vs OCR median $2,386). The CCR-to-RCR gap has effectively closed, with some RCR launches pricing at or above CCR levels. This is a structural shift driven by elevated RCR land costs and new launch repricing. Use this in client conversations: RCR projects today are priced where CCR projects were just a few years ago.

ABSD rates (unchanged since April 2023):

- Singapore Citizens: 0% (1st), 20% (2nd), 30% (3rd+)

- PRs: 5% (1st), 30% (2nd), 35% (3rd+)

- Foreigners: 60% (any property)

EC Eligibility Quick Reference

With three ECs launching in H2 2026, agents will field eligibility questions regularly. Here are the key criteria:

- Citizenship: At least one buyer must be a Singapore Citizen. The other buyer (in a couple) must be an SC or PR.

- Household income ceiling: $16,000 per month.

- Age: Minimum 21 years old.

- Property ownership: Must not own any private property locally or overseas. If disposing of an existing HDB flat, the 30-month wait-out period applies (from the date of disposal) before the EC can be purchased.

- Resale restrictions: Cannot sell on open market for first 5 years. After year 5, can sell to SCs and PRs only. After year 10, fully privatised with no restrictions.

Head-to-Head: Which Projects Compete

Clients will compare projects. Here are the four key competitive matchups and how to position each one.

Battle 1: Vela Bay vs Lakeside Drive Condo

Both target OCR/RCR buyers in the $2,300 to $2,800 range, but the pitch is different.

- Vela Bay sells the East Coast lifestyle and direct TEL access. Better for buyers who value recreation, established food options, and beach proximity.

- Lakeside Drive sells the Jurong Lake District future and multi-line MRT convergence. Better for buyers who want long-term capital appreciation from a district-level transformation.

Positioning tip: If your client is an owner-occupier who wants lifestyle now, lean Vela Bay. If your client is an investor with a 7 to 10 year horizon, lean Lakeside Drive.

Battle 2: Thomson View vs Chuan Grove

Both are mega-developments in mature RCR/OCR neighbourhoods, competing for the upgrader dollar.

- Thomson View (~1,240 units, $2,300-$2,600 psf) offers more competitive pricing and a stronger MRT connectivity story (triple MRT access plus CRL interchange by 2030).

- Chuan Grove (~1,055 units, $2,600-$2,800 psf) benefits from the established Serangoon neighbourhood, Nex mall, and proximity to Serangoon interchange.

Positioning tip: Thomson View is the value play with bigger upside potential. Chuan Grove is the safe, established neighbourhood pick. Match to your client's risk appetite.

Battle 3: Hudson Place vs Dover Road

Both sit in the one-north/Buona Vista corridor (D5), targeting the same pool of tech professionals and NUS-linked buyers.

- Hudson Place (~325 units, ~$2,200+ psf) is smaller scale with a confirmed developer and pricing estimates.

- Dover Road (~625 units, TBA) is larger but details are still emerging.

Positioning tip: For clients who want certainty and earlier entry, push Hudson Place. Keep Dover Road as a backup if clients want to wait and compare.

Battle 4: Tengah Garden vs Lentor Gardens

Both target first-time buyers and upgraders at the most accessible price points.

- Tengah Garden (~860 units, $1,600-$2,000 psf) is the pioneer project in a brand-new town. Lower entry point but unproven neighbourhood.

- Lentor Gardens (499 units, $2,200+ psf) sits in an established cluster with TEL access and proven demand.

Positioning tip: Tengah for clients who want lowest quantum and are comfortable being early adopters. Lentor for clients who prefer proven track records.

MRT Connectivity Quick Reference

MRT proximity is one of the top three factors buyers consider. Here is every project's connectivity profile, including upcoming TEL, CRL, and JRL catalysts that will boost future value.

| Project | Nearest MRT | Line(s) | Walk Time | Upcoming Catalysts |

|---|---|---|---|---|

| Vela Bay | Bayshore (TE29) | TEL | Adjacent | TEL Stage 5 (Bedok South, Sungei Bedok) opening H2 2026 |

| Tengah Garden | Hong Kah (future) | JRL | TBA | JRL construction in progress |

| Hudson Place | one-north (CC23) | CCL | ~15 min (shuttle) | Complimentary shuttle service provided |

| Lentor Gardens | Lentor (TE5) | TEL | ~5 min | TEL fully operational |

| 132 Sophia Road | Dhoby Ghaut (NS24/NE6/CC1) | NSL, NEL, CCL | ~5 min | 4 MRT lines within walking distance |

| Lakeside Drive | Lakeside (EW26) | EWL | Adjacent | JRL at Jurong East (delayed from 2028), CRL network expansion (2030s) |

| Dorset Road | Farrer Park (NE8) | NEL | ~5 min | N/A |

| Thomson View | Upper Thomson (TE8) / Bright Hill (TE7) | TEL | ~8 min | Bright Hill becomes TEL-CRL interchange (2030) |

| Chuan Grove | Lorong Chuan (CC14) | CCL | ~5 min | Serangoon North CRL station (2030) |

| Hougang Central | Hougang (NE14) | NEL | Direct (above station) | CRL interchange by 2030 |

| Lentor Central (Plot 4) | Lentor (TE5) | TEL | ~8 min | TEL fully operational, established precinct connectivity |

| Telok Blangah Road | Telok Blangah (CC28) | CCL | ~8 min | Greater Southern Waterfront transformation |

| Holland Link | Holland Village (CC21) | CCL | ~10 min | Holland Village MRT extension |

| Bukit Timah Road | Newton (NS21/DT10) | NSL, DTL | ~5 min | Dual-line interchange access |

| Dunearn Road | Sixth Avenue (DT7) | DTL | ~5 min | Future Turf City CRL station |

| Chencharu Close | Khatib (NS14) | NSL | ~3 min | Integrated bus interchange within development |

| Upper Thomson Parcel A | Springleaf (TE4) | TEL | Adjacent | TEL fully operational |

| Keppel Bay Plot 6 | HarbourFront (NE1/CC29) | NEL, CCL | ~8 min | Greater Southern Waterfront transformation |

The TEL and CRL story in one sentence: TEL is largely complete, with Stage 5 finishing the line in H2 2026. CRL Phase 1 opens in 2030 with 12 stations (including the key Bright Hill TEL-CRL interchange), and Phase 2 follows in 2032 extending west to King Albert Park and Clementi.

Market Risks and Client Objections

A complete cheat sheet should not just give you selling points. It should prepare you for pushback. Here are the key risks clients will raise and how to address each one.

1. "Should I wait for prices to come down?"

Structural factors suggest this is unlikely in the near term. Land costs from 2024 and 2025 GLS tenders are at record levels, and construction costs remain elevated. Developers cannot sell below their break-even cost, and the supply pipeline is limited. However, it is fair to tell clients that individual projects may offer early-bird or VVIP discounts during the first preview weekend. The time to act is during launch, not after.

2. Interest rate sensitivity

Mortgage rates have stabilised around 1.5% to 2% for packages pegged to SORA. If rates rise, monthly repayments increase and affordability tightens. Run the numbers for your clients at both current rates and a stress-tested rate of 3.5% to 4% so they know their worst-case monthly commitment. The Total Debt Servicing Ratio (TDSR) of 55% already stress-tests at 4%, so clients who pass TDSR can generally handle moderate rate increases.

3. Q3 launch clustering risk

Q3 2026 will see Thomson View (~1,240 units), Chuan Grove (~1,055 units), and Hougang Central Residences (~835 units) all coming to market around the same time. That is over 3,000 units in one quarter. When supply clusters like this, individual take-up rates may soften as buyers spread across multiple options. For agents, this means clients will comparison-shop heavily, and urgency at any single launch may be lower than at standalone launches. Use this to your advantage: position yourself as the agent who has done the comparison work already.

4. Global economic headwinds

Singapore's property market is not immune to global conditions. A recession in major economies, trade disruptions, or a sudden tightening cycle could weigh on buyer sentiment. The counter-argument is that Singapore's safe-haven status historically attracts capital during uncertainty, and the domestic upgrader market (which drives most new launch demand) is less correlated with global cycles. Still, advise clients to buy within their means and not over-leverage on the assumption that prices will only go up.

How to Prepare for Launch Season

The agents who close deals during launch season are the ones who prepare before it starts. Here are five things to do this week.

1. Pre-register at every showflat

Vela Bay and Tengah Garden Residences both open VVIP previews in April 2026. Register early. VVIP slots go fast and give your clients first-mover access to the best stack and floor selections.

2. Segment your client list now

Go through your contacts and tag them by:

- Budget range (quantum, not just PSF)

- Buyer type (first-timer, upgrader, investor, PR)

- Location preference

- Timeline (ready to commit in Q2 vs later in the year)

This lets you send targeted recommendations instead of blasting every client with every launch.

3. Know the numbers cold

For each project you plan to pitch, have these ready:

- Entry quantum (smallest unit type x estimated PSF)

- Monthly mortgage estimate (at current rates around 1.5% to 2%)

- ABSD implications for the buyer's specific profile

- SSD holding period reminder (four years now)

- Comparable resale PSF in the same district

4. Build your comparison toolkit

Clients will ask "why this one over that one?" Prepare two to three comparison slides or messages for competing projects. The head-to-head section above gives you the positioning angles.

5. Follow up systematically

Launch season means high volume. If you are managing more than 10 active prospects across multiple launches, use a CRM to track who is interested in what, when you last contacted them, and what their next step is. Missing a follow-up during launch week can cost you a deal.

Never lose a launch-season lead again

PropPal turns your WhatsApp conversations into a structured CRM with AI-powered follow-up reminders.

Try PropPal Free for 7 Days Setup takes 5 minutes. Cancel anytime.Key Takeaways

- Q2 2026 brings at least five confirmed launches led by Vela Bay and Tengah Garden Residences, both opening VVIP previews in April.

- Q3 2026 and beyond features mega-developments Thomson View (~1,240 units), Chuan Grove (~1,055 units), and Hougang Central (~835 units), plus Telok Blangah Road (~745 units) as the first private launch on the Greater Southern Waterfront.

- The EC pipeline is stacked. Three EC projects are launching in H2 2026 and early 2027: Senja Close, Sembawang Road, and Woodlands Drive 17 (~980 units). EC-eligible buyers will have options across multiple districts.

- Price floors have risen structurally. Land costs, construction costs, and limited completions all support current and higher PSF levels. The CCR-to-OCR premium has compressed to single digits.

- The CRL is the next major connectivity catalyst. Phase 1 (2030) creates a TEL-CRL interchange at Bright Hill. Phase 2 (2032) extends west to King Albert Park and Clementi. Projects near these future stations carry extra upside.

- Be ready for client pushback. Prepare talking points on interest rate sensitivity, the Q3 launch clustering effect, and global economic headwinds. Buyers will be cautious, and the agents who address objections directly will close more deals.

- Preparation beats reaction. Pre-register at showflats, segment your client list by budget and buyer type, and have comparison talking points ready before launch day.

Frequently Asked Questions

What are the biggest new condo launches in Singapore Q2 2026?

The largest Q2 2026 launch is Tengah Garden Residences with approximately 860 units, followed by Lentor Central Plot 4 (~580 units, H2 2026), Vela Bay (515 units), and Lentor Gardens Residences (499 units). All are 99-year leasehold developments launching between April and late 2026.

What is the expected PSF price range for new condos in Singapore in 2026?

New launch prices in 2026 range from approximately $1,900 to $2,500 psf in the OCR, $2,400 to $2,800 psf in the RCR, and $2,800 to $3,300+ psf in the CCR. Executive Condominiums are pricing between $1,650 and $1,770 psf. These ranges are based on recent launch benchmarks and verified market data as of early 2026.

Which upcoming Singapore condos are near new MRT stations?

Vela Bay is adjacent to Bayshore MRT (TEL, opened 2024) and benefits from TEL Stage 5 completing in H2 2026. Thomson View will be near the future Bright Hill TEL-CRL interchange (2030). Lakeside Drive Condo is adjacent to Lakeside MRT and will benefit from JRL connectivity at nearby Jurong East by 2028.

What are the current ABSD rates in Singapore for 2026?

Singapore Citizens pay 0% ABSD on their first property, 20% on the second, and 30% on the third and beyond. Permanent Residents pay 5% on the first, 30% on the second, and 35% on the third and beyond. Foreigners pay 60% on any residential property. These rates have been in effect since April 2023.

How has the Seller's Stamp Duty changed in 2025?

Since July 2025, the SSD holding period was extended from three years to four years. Rates increased by four percentage points per tier: 16% within year one, 12% within year two, 8% within year three, and 4% within year four. The previous rates were 12%, 8%, 4%, and 0% respectively.

Sources

- URA Q4 2025 Real Estate Statistics

- ERA 4Q 2025 URA Private Quarterly Report

- ERA 4Q 2025 Press Release: Private Home Demand Outlook for 2026

- MAS: SSD Changes July 2025

- IRAS: ABSD Official Rates

- Stacked Homes: 2026 New Launch Outlook

- 99.co: Full List of New Condo Launches 2026

- PropertyGuru: Upcoming New Launch Condo 2026

- LTA: Thomson-East Coast Line

- LTA: Cross Island Line

- Vela Bay on NewLaunches.sg

- Tengah Garden Residences Official Site

- Hudson Place Residences Official Site

- Lakeside Drive Condo Official Site

- Chuan Grove Official Site

- EdgeProp: Sing Holdings Prepares for Chuan Grove

- EdgeProp: UOL and CapitaLand Acquire Thomson View

- EdgeProp: Lentor Central GLS Plot 4 Top Bid at $1,278 psf ppr

- Condo.com.sg: Higher New Launch Prices Expected in 2026